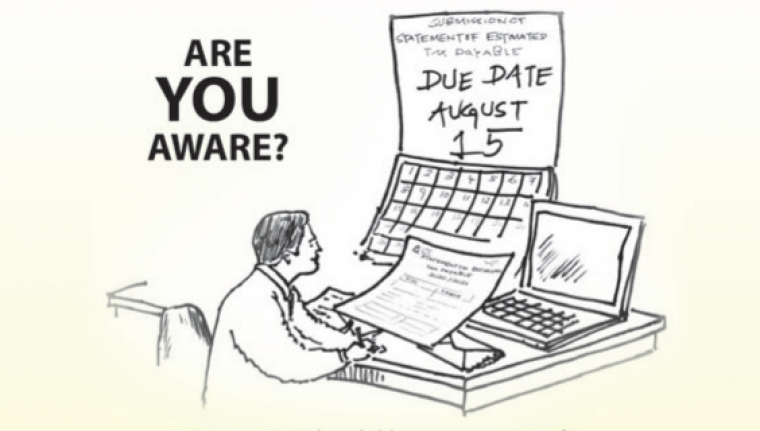

Why 15th of August is so important ?

In terms of Sections 90 and 91 of the Inland Revenue Act, No. 24 of 2017 (IR Act) , a person who is an instalment payer shall pay income tax based on the estimated taxable income by quarterly instalments on the 15th of August, 15th of November and 15th of February in that year of assessment and the 15th of May of the next succeeding year of assessment and is required to submit a Statement of Estimated Tax Payable (SET) by the date for payment of the first tax instalment.

Accordingly, any instalment payer shall file the SET and pay the 1st instalment for the year of assessment 2020/2021 on or before the 15th of August 2020.

The SET consists of two parts, PA RT I and PART II. All instalment payers should complete PART I and PART II of the SET.

The SET consists of two parts, PA RT I and PART II. All instalment payers should complete PART I and PART II of the SET.

However, any individual who has ONLY employment income and already given the consent to deduct Advance Personal Income Tax (APIT) on such employment income should only complete PART II of the SET (Declaration) and submit to Inland Revenue Department (IRD)

Issuance and Submission

Issuance

SET shall be issued by the Commissioner General of Inland Revenue to persons who are chargeable with income tax. Those who have not received the SET (Individuals whose estimate income exceeds more than Rs. 3,000,000 for the Year of Assessment 2020/2021 could obtain a SET from the Taxpayer Services Unit at the IRD Head Office or from any Regional Office.

Submission

Duly completed SET Form can be furnished to the Central Document Management Unit (CDMU) at the IRD Head Office or to any Regional Office.

OR

SET Form can be sent through registered post to the Commissioner, Central Document Management Unit, Inland Revenue Department, Chittampalam A Gardiner Mawatha, Colombo 02.

How to calculate

How to calculate

As per the Section 90(3) of the Act, installment tax payable is to be calculated using following formula:

Installment Payment = (A - C) / B

A =Estimated Tax Payable

B =Number of installments remaining including the current installment

C = Tax payments prior to that installment

Penalty for late filing and submitting of false or misleading SET Form

Penalty for late filing and submitting of false or misleading SET Form

- A person who fails to submit the SET on or before the due date, shall be liable to pay a penalty under Section 185 of the IR Act.

- Accordingly, a person who fails to comply with a request for information properly made under this Act, within the specified time, shall be liable for a penalty of an amount not exceeding one million.

- The SET form considered as a statement to a tax officials and penalty will imposed under section 181 of the IR Act on false or misleading statement.

Legal Actions for evading instalment payments

Following legal actions can be contemplated against any person who has willfully evaded instalment payments.

1.Penalty for nonpayment /late payment - (Under Section 179 (2) of the IR Act)

A person who fails to pay all or part of an instalment required under this Act, within 14 days of the due date for the instalment shall be liable to a penalty equal to 10% of the amount of tax due but not paid

2.Interest on default - (Under Section 159 (1) of the IR Act)

In the event of a default of an instalment or part thereof, 1.5% interest per month or part of a month could be charged on such default instalment or part of the instalment.

We provide online support service to fill your SET form alone with the guidance of Tax Experts.Visit www.taxadvisor.lk/tax-agent